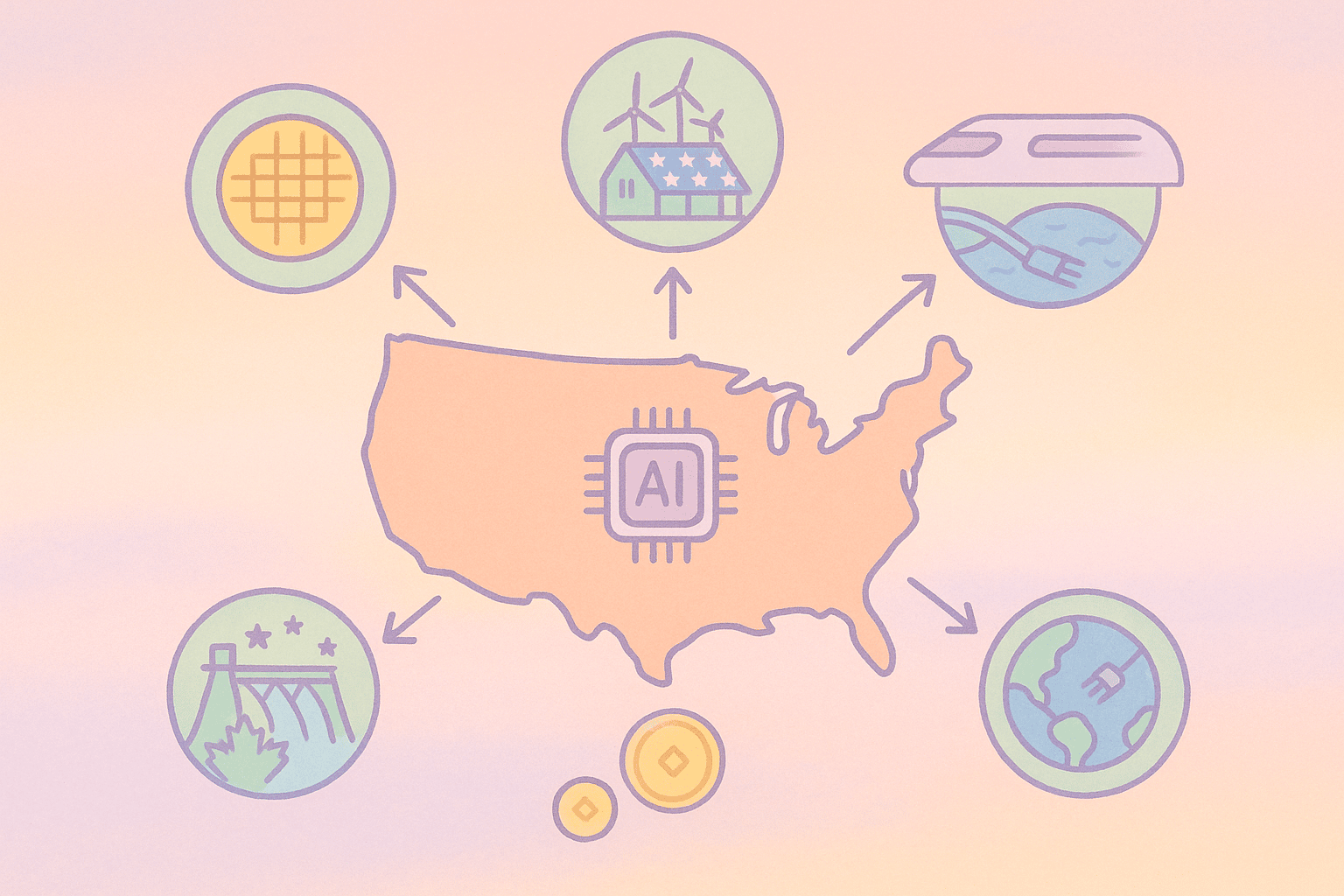

TL;DR: The AI boom is quietly reshaping Earth's resource consumption at unprecedented scale. U.S. hyperscale data centers now withdraw 66 billion liters of water annually[7] (triple 2014 levels) while Google alone consumed 30.8 TWh of electricity in 2024, roughly doubling its 2020 usage[8]. By 2026, global data center demand (much of it AI-driven) could reach 1,050 TWh, roughly double today's total and on par with Japan, the world's 5th-largest electricity consumer[9]. Yet companies continue paying these massive environmental costs because AI delivers immediate productivity gains: call center agents see 14% efficiency boosts, and early adopters save 5.4% of their weekly work hours[10][11]. The race is now on to power this transformation through fusion partnerships, small nuclear reactors, and 24/7 renewable contracts before regulators impose hard limits.

Behind every ChatGPT conversation, every Claude analysis, and every GPT-powered code completion lies an invisible infrastructure consuming resources comparable to mid-sized nations. While the tech world celebrates AI's capabilities, a quieter revolution is unfolding in utility consumption, one that's forcing humanity to rethink how we power and cool the digital transformation.

The numbers tell a story of exponential resource hunger that few anticipated. What started as clever algorithms has evolved into an industrial operation demanding municipal-scale water supplies and electricity grids that dwarf those of major cities.

Why This Matters Now

The Scale: Global data center consumption could reach nation-scale levels by 2026, with AI driving exponential growth that could strain utilities worldwide

The Timeline: Current energy deals and fusion partnerships suggest the industry knows traditional power sources won't scale

The Reckoning: EU regulations and local water restrictions signal the end of consequence-free expansion

The Invisible Thirst: How AI Learned to Drink

The most overlooked aspect of AI's environmental impact isn't carbon emissions. It's water consumption. Every GPU cluster generating tokens requires massive cooling systems that literally evaporate thousands of gallons daily into the atmosphere.

This isn't just a statistical curiosity. It's reshaping local politics. In drought-prone regions, the arrival of a new AI campus can strain municipal water supplies that took decades to develop. A single Google facility averages 550,000 gallons daily[17], roughly equivalent to the water needs of a town of 15,000 people.

Stanford's "And the West" project[7] reveals the geographic concentration within the U.S.: 84% of this domestic water usage flows to the largest GPU farms, creating localized stress that national averages mask. Communities that welcomed tech investment now find themselves choosing between economic growth and water security.

Why AI Needs So Much Water

Evaporative Cooling: GPUs generate intense heat that traditional air cooling can't handle at scale. Water-cooled systems use evaporation to carry away thermal energy, literally turning liquid water into vapor that dissipates into the atmosphere

Continuous Operation: Unlike office buildings with day/night cycles, AI clusters run 24/7 at full capacity, requiring constant cooling

Efficiency Trade-offs: More water-efficient cooling exists, but it's expensive and reduces computational density

The water crisis represents just half the story. While communities debate water rights, a parallel crisis unfolds in electricity grids worldwide.

The Great Power Hunger: When Code Consumes Countries

Google's 2024 environmental filing contains a number that should concern anyone thinking about AI's long-term sustainability: 30.8 TWh of electricity consumption, up from 14.4 TWh just four years earlier[8]. This isn't gradual growth. It's exponential demand that's forcing fundamental questions about how we power civilization.

MIT analysts project the entire data center sector will hit 1,050 TWh by 2026[9], enough electricity to rank fifth globally if data centers were their own country, just behind Russia and well ahead of Germany or Canada.

This exponential growth trajectory is forcing the tech industry to think beyond traditional power procurement. When your electricity needs double every few years, you can't simply buy more renewable energy credits and call it sustainable. You need entirely new approaches to baseload power generation, and fundamental improvements in computational efficiency. The recent shift toward specialized AI chips offers one path forward, with purpose-built inference accelerators delivering 4-8× better energy efficiency than traditional GPUs.

The New Energy Playbook: From Fusion Dreams to Fission Reality

Faced with unsustainable growth in power demand, tech giants are pioneering energy strategies that read like science fiction. The most audacious moves involve technologies that didn't exist at commercial scale just years ago.

How Tech Giants Are Reinventing Power Generation

The three emerging strategies for powering AI at unprecedented scale

Fusion Partnerships: The 2028 Bet

Microsoft partnered with Helion for 50 MW fusion power by 2028, while Google signed a 200 MW offtake with Commonwealth Fusion Systems

Small Modular Reactors: On-Site Nuclear

Oklo secured letters of intent for 750 MW across two unnamed hyperscalers, sized specifically for data center footprints

24/7 Renewable Matching

Record 62 GW of corporate solar and wind PPAs signed in 2024, plus Google's first corporate geothermal deal in Taiwan

Advanced Grid Integration

Smart load balancing and demand response systems to maximize renewable utilization and minimize grid stress

The fusion partnerships represent the most ambitious bet. Microsoft's deal with Helion[1] and Google's agreement with Commonwealth Fusion Systems[2] aren't just energy contracts. They're technology development partnerships that could reshape how humanity generates power, if projects hit their stated 2028-30 milestones.

But fusion remains experimental. The near-term solution lies in Small Modular Reactors (SMRs), where Oklo's 750 MW in signed letters of intent[3] represents the first serious attempt to locate nuclear power generation directly at data center sites. This eliminates transmission losses and provides the 24/7 baseload power that solar and wind can't reliably deliver.

Why Nuclear Makes Sense for AI

Baseload Power: Unlike solar and wind, nuclear provides constant electricity that matches AI's 24/7 computational demands

Carbon-Free: Zero operational emissions while delivering the massive scale AI requires

Site Flexibility: SMRs can be located directly at data centers, eliminating transmission infrastructure

Long-Term Stability: Decades-long operational cycles match the investment horizons of major AI infrastructure

Meanwhile, the renewable strategy focuses on "hourly matching," using smart contracts and battery storage to ensure every kWh of AI computation is matched with clean generation. This approach drove record corporate renewable procurement: 62 GW of corporate solar and wind PPAs signed in 2024[4]. Google's 700 MW Oklahoma solar project[5] and Taiwan geothermal deal[6] represent this approach at scale.

The Regulatory Reckoning: When Governments Draw Lines

The era of consequence-free AI expansion is ending. European regulators are pioneering restrictions that foreshadow global policy changes, while local communities implement water use moratoria that directly impact facility planning.

The EU's sustainability registry[15] represents the first mandatory reporting regime, requiring any data center above 500 kW to disclose water usage, power consumption, and carbon metrics annually. But disclosure is just the beginning.

Energy Commissioner Dan Jørgensen's June 2025 announcement[16] confirms Brussels is drafting efficiency packages that could mandate live public dashboards and set minimum Power Usage Effectiveness (PUE) and Water Usage Effectiveness (WUE) thresholds. These aren't suggestions. They're coming regulatory requirements that could force facility redesigns.

The Coming Regulatory Wave

How governments are preparing to limit AI's resource consumption

First mandatory sustainability reports due for data centers >500 kW across European Union

Proposed EU rules setting minimum PUE/WUE standards with public dashboard requirements

Local moratoria in Oregon, Arizona, and other water-stressed regions blocking new AI facilities

More jurisdictions including data centers in carbon pricing schemes and renewable energy mandates

The pattern is clear: disclosure leads to transparency, transparency reveals problems, and problems trigger restrictions. Companies that wait for regulations will find themselves scrambling to retrofit facilities or relocate operations.

Local water restrictions represent the most immediate threat. Communities that initially welcomed tech investment are discovering that a single AI campus can stress municipal water systems built for entirely different uses. The political backlash is forcing facility developers to consider water-efficient cooling systems that were previously deemed too expensive.

The Regulatory Arbitrage Window Is Closing

Current Strategy: Many companies locate facilities in regions with minimal environmental oversight, externalizing climate costs to local communities

Coming Reality: Coordinated international standards will eliminate jurisdiction shopping, forcing all facilities to meet similar sustainability requirements

Investment Implication: Early investments in efficient infrastructure provide competitive advantages as regulatory pressure intensifies globally

The Uncomfortable Questions We're Not Asking

As AI infrastructure scales toward national-level resource consumption, several critical questions remain largely unaddressed by industry leaders and policymakers alike.

Local Impact vs. Global Benefits: Companies pledge to be "water-positive" through global offsets, but this doesn't help arid communities facing immediate water stress from new AI facilities. Should local resources subsidize global AI capabilities? How do we balance technological progress against environmental justice?

The Baseload Gap: Even with record renewable energy investments, intermittent sources can't provide the 24/7 baseload power that AI clusters require. If fusion and SMR deployment lags, what fills the gap? Coal and natural gas plants? Extended nuclear reactor lifespans? The clean energy transition timeline may not match AI growth curves.

Inference Optimization Limits: Current research focuses on architectural improvements to reduce energy per token, but physics imposes fundamental limits. The evolution from power-hungry transformers to more efficient architectures shows promise, yet we're still orders of magnitude away from biological efficiency. What happens when we reach the thermodynamic floor of computation? Do we accept higher per-query costs, or do usage patterns need to change?

Productivity Diminishing Returns: Early AI adoption shows dramatic efficiency gains, with research showing particularly strong benefits for novice workers[10]. However, these effects vary significantly across roles and experience levels, and may not be sustainable at scale. As AI becomes ubiquitous, will marginal productivity improvements justify exponentially growing infrastructure costs? The economic justification for massive resource consumption assumes continued productivity acceleration.

Democratic Decision-Making: Who decides whether humanity should dedicate nation-scale resources to AI infrastructure? These choices affect everyone but are currently made by a handful of tech executives and their investors. Do we need new governance mechanisms for civilization-scale technological decisions?

Market Watch: Who Gains, Who Strains

The "water and watts" squeeze is reshaping public market valuations and long-term prospects across the AI infrastructure stack. Companies that solve the baseload-clean-power puzzle early can widen AI margins and build a sustainable competitive advantage, while laggards may face compounding utility bills and regulatory penalties.

Here's a breakdown of which companies are best positioned to navigate these environmental crosscurrents:

Hyperscale Giants: Google (GOOGL) faces the highest immediate exposure, running the world's second-largest data center fleet while being first in line for EU dashboard costs and water offset requirements. Yet its leadership in AI and aggressive renewable energy deals provide a path to mitigate these risks. Microsoft (MSFT) commands a "clean energy premium" with its Helion fusion partnership and massive renewable contracts, though its expansion in water-stressed regions like Arizona remains a key risk factor. Amazon (AMZN) benefits from soaring AWS inference demand but faces margin pressure if its renewable PPA acquisitions can't keep pace with its exponential load growth.

Data Center REITs: The infrastructure landlords face a capital expenditure crunch. Equinix (EQIX) must retrofit evaporative cooling towers to more efficient (and expensive) closed-loop chillers in drought-prone states, pressuring near-term margins. Digital Realty Trust (DLR) could benefit if EU regulations steer tenants toward its modern, efficient facilities that already meet anticipated standards.

Energy Infrastructure: NextEra Energy (NEE) emerges as a clear winner, perfectly positioned to capitalize on the record-setting corporate PPA boom. Its extensive renewable portfolio and development pipeline make it a primary partner for hyperscalers seeking to offset their consumption. NuScale Power (SMR) rides speculative momentum as the first NRC-approved small modular reactor design, positioning it as a potential "GPU-companion" for on-site data center power, though significant financing and deployment hurdles remain. Hardware diversification toward specialized AI chips also creates new investment dynamics as companies move beyond Nvidia's GPU ecosystem.

Key Market Catalysts to Watch

Hard EU Water Caps: Would impact GOOGL, AMZN, and MSFT first, with retrofit costs potentially passed through to EQIX and DLR tenants, testing the resilience of their business models.

Helion 2028 Milestone: A breakthrough or delay on fusion energy will significantly swing sentiment on MSFT's long-term energy strategy and the viability of the "nuclear for AI" trade.

Corporate PPA Pricing: Every incremental contract favors renewable developers like NEE, but margins could compress as supply eventually scales to meet the enormous demand.

The financial outlook mirrors the climate ledger: companies solving baseload clean power early can expand AI margins, while laggards face compounding utility and compliance costs.

The Path Forward: Efficiency or Limits?

The AI industry faces a fundamental choice: engineer its way to sustainability or accept external limits on growth. Current trends suggest both paths will be necessary.

On the efficiency front, promising developments include:

Specialized AI Chips: The shift away from general-purpose GPUs toward purpose-built inference accelerators is dramatically reducing energy costs. OpenAI's recent move to Google's TPUs for inference workloads demonstrates how alternative chips can cut costs by 4-8× per token, slashing API prices by 80% while reducing power consumption. This trend toward architectural diversity reflects how different AI approaches require different hardware optimizations, as the industry moves beyond Nvidia's one-size-fits-all GPU dominance.

Sparse Architectures: Next-generation models activate only relevant neural network components for each query, dramatically reducing computational overhead. Instead of using every parameter for every request, these systems intelligently route computations to specialized model segments.

Advanced Cooling Systems: Innovative thermal management including immersion cooling, direct-to-chip liquid cooling, and waste heat recovery systems that can capture and repurpose thermal energy for adjacent facilities or district heating networks.

Software-Hardware Co-optimization: Purpose-built inference accelerators designed specifically for transformer architectures or emerging alternatives like state space models, optimizing the entire computational pipeline rather than adapting general-purpose hardware.

But efficiency gains may not match demand growth. If AI capabilities continue expanding exponentially while per-operation efficiency improves linearly, total resource consumption still explodes.

The alternative, accepting limits, requires unprecedented coordination between technological ambition and planetary boundaries. This might involve:

- Usage pricing that reflects true environmental costs

- Facility restrictions in water-stressed or carbon-intensive regions

- Efficiency mandates that force architectural improvements

- Democratic oversight of major infrastructure decisions

The companies making massive fusion and nuclear investments are essentially betting that technological solutions will arrive before regulatory limits become constraining. It's a high-stakes gamble with global infrastructure implications.

Whether through breakthrough efficiency or imposed restrictions, the era of consequence-free AI expansion is ending. The question isn't whether change is coming; it's whether the industry will lead that change or have it imposed from outside.

The hidden climate costs of AI are becoming visible. What we do with that visibility will determine whether artificial intelligence becomes humanity's greatest tool or its most expensive mistake.

Sources & References

Key sources and references used in this article

| # | Source | Outlet | Date | Key Takeaway |

|---|---|---|---|---|

| 1 | Helion Energy Helion Team | 10 May 2023 | First commercial fusion power purchase agreement targeting 50 MW delivery by 2028 | |

| 2 | Axios Axios Richmond Staff | 30 Jun 2025 | Google's 200 MW fusion power offtake agreement with Commonwealth Fusion Systems | |

| 3 | Oklo Inc. Oklo Press Office | 18 Nov 2024 | Letters of intent for SMR deployment to two major hyperscale customers | |

| 4 | LevelTen Energy LevelTen Team | 12 Feb 2025 | Record 62 GW of corporate renewable energy PPAs signed in 2024 | |

| 5 | Smart Energy Decisions Smart Energy Staff | 15 Jan 2025 | Major solar power purchase agreement supporting AI infrastructure expansion | |

| 6 | Google Blog Google Sustainability Team | 22 Apr 2025 | First corporate geothermal PPA in Taiwan plus Oklahoma solar project details | |

| 7 | Stanford And the West Stanford Research Team | 14 Apr 2025 | 66 billion liters annual water consumption by hyperscale data centers, 84% from GPU farms | |

| 8 | Google Google Sustainability Team | May 2025 | Google's electricity consumption reached 30.8 TWh in 2024, up from 14.4 TWh in 2020 (p. 17) | |

| 9 | MIT News MIT Sustainability Team | 17 Jan 2025 | Projection of 1,050 TWh total data center consumption by 2026 | |

| 10 | NBER Brynjolfsson, Li, Raymond | Apr 2023 | Call center study showing 14% productivity improvement with AI copilots, 34% for novices | |

| 11 | Federal Reserve Bank of St. Louis St. Louis Fed Research | Feb 2025 | Survey finding 5.4% weekly work hours saved by generative AI users | |

| 12 | Medium Kasper Groes Albin Ludvigsen | 15 Mar 2024 | Analysis estimating GPT-3 training emissions at 552 tons CO₂ equivalent | |

| 13 | arXiv Chen et al. | 14 Jan 2025 | Study confirming linear relationship between context length and inference energy consumption | |

| 14 | Nature News Nature News Team | Mar 2025 | Analysis of AI energy consumption patterns and environmental impact projections | |

| 15 | European Commission EU Energy Directorate | 15 Mar 2024 | Mandatory sustainability reporting for data centers above 500 kW starting 2025 | |

| 16 | Reuters Reuters Staff | 12 Jun 2025 | Upcoming EU efficiency package with mandatory PUE/WUE thresholds announced by Commissioner Jørgensen | |

| 17 | University of Illinois CEE Civil Engineering Research | 8 Nov 2024 | Analysis showing Google data centers average 550,000 gallons daily water consumption | |

| 18 | Yahoo Finance Historical Data Market Data | 3 Jul 2025 | GOOGL closing price $179.53 on July 3, 2025 | |

| 19 | DataCenterDynamics DCD Research Team | Jan 2025 | Analysis of data center power consumption providing context for REIT infrastructure investments | |

| 20 | Reuters Reuters Energy Desk | 1 Jul 2025 | Analysis of renewable energy demand from data center expansion and market implications | |

| 21 | Reuters Reuters Energy Team | 24 Jul 2024 | NextEra executives project massive renewable energy demand growth driven by data center expansion | |

| 22 | Reuters ESG Watch Reuters Sustainability Team | 16 Jun 2025 | Analysis of environmental costs and regulatory risks facing data center operators |

Last updated: July 6, 2025